A Builder's Views on Stablecoin Exchanges

In 1993, Eric Hughes wrote that privacy is not secrecy, it is the power to selectively reveal oneself to the world. The cypherpunks who built on that principle spent the following decade engineering the cryptographic primitives that would eventually become digital money: proof of work, smart contracts, trustless settlement. They were not building for institutions. They were building for individuals who had decided that digital autonomy was worth the engineering effort.

Thirty years later, the stablecoin is the most adopted product that lineage produced and also its most uncomfortable compromise. A dollar-pegged token issued by a regulated entity, backed by Treasury bills, redeemable only through a licensed intermediary, is not what the cypherpunks had in mind. And yet it is what millions of people in high-inflation economies are using to escape monetary systems that failed them, what institutions are using to move capital across borders at a fraction of the cost, and what DeFi protocols are using as the unit of account for a parallel financial system being built in public.

This paper looks at stablecoin exchanges from the perspective of a builder, not as a policy question nor investment thesis, but as a set of engineering and market structure problems with identifiable solutions. It traces the cypherpunk inheritance through the institutional compliance framework that now governs stablecoin issuance, examines why stablecoins that claim identical pegs are not actually fungible, maps the arbitrage flows that exploit this non-fungibility and the ones that could correct it, and asks what the growing adoption of dollar-denominated digital assets implies for the global monetary order.

The argument that runs beneath the analysis: the inefficiency of on-chain stablecoin exchange is not a residual problem waiting for markets to mature. It is a structural feature being actively extracted. The infrastructure to price and clear that inefficiency already exists in its components. The question is whether it gets assembled.

Keywords: stablecoin, fungibility, arbitrage, adoption

Section Summaries

Section 1 — The Cypherpunk Alignment Thesis vs Institutional Control: The cypherpunk movement built the cryptographic foundations of digital cash on the premise that privacy is an engineering problem, not a political negotiation. Nowadays, every fiat-backed stablecoin requires a licensed, regulated entity as counterparty, and the GENIUS Act has codified this into law. The result is a layered topology: the base money layer is centralized by design, the on-chain transfer layer is permissionless by design, and individual autonomy exists in the gap between them.

The section maps the user categories who navigate this gap and closes on a taxonomy of what makes stablecoin exchange non-uniform across segments, which the following sections unpack mechanically.

Section 2 — The Fungibility Issue: Two stablecoins claiming identical dollar pegs are not the same instrument. The spread between them encodes three measurable variables: information asymmetry, risk differentiated by collateral and governance structure, and barriers to redemption access that vary by user type. A fair exchange rate is a function of all three. In practice, the 1:1 convention holds in calm conditions and breaks exactly when accuracy matters.

The section establishes that peg stability is a function of arbitrage efficiency, and the difference between quality arbitrage and toxic flow. Oracle feeds are the instrument that makes this distinction legible on-chain.

Section 3 — Forex & Adoption: Stablecoins pegged to the US dollar represent 97% of all stablecoin issuance. The euro, the world’s second reserve currency, holds less than 1% of the on-chain stablecoin market, a structural consequence of regulatory sequencing and DeFi liquidity bootstrapping dynamics rather than builder preference. In economies where local monetary infrastructure has failed, stablecoins are the financial infrastructure. The dollar monoculture this produces is simultaneously an amplifier of US monetary hegemony and a set of rails that adversarial actors can access permissionlessly.

Whether this dynamic accelerates dollar dominance or gradually fragments it into competing on-chain currency blocs is the question the section explores without formally answering.

Section 1: The Cypherpunk Vision vs Institutional Control

1.1 Code is Law: The Intellectual Foundations of Digital Privacy

The tension that animates this section was articulated thirty years before it became legally relevant. In 1993, Eric Hughes published A Cypherpunk’s Manifesto, declaring:

“Cypherpunks write code. We know that someone has to write software to defend privacy, and since we can’t get privacy unless we all do, we’re going to write it.”

The statement was both a technical roadmap and a political claim: that privacy, in a digital world, would not be granted by institutions but engineered by individuals.

This ethos produced a generation of builders whose work directly seeded the digital economy. Adam Back’s Hashcash (1997) introduced computational scarcity without a trusted issuer. Hal Finney, who received the first Bitcoin transaction from Satoshi Nakamoto, had developed Reusable Proof-of-Work (RPOW) in 2004 as a prototype for digital cash built on Nick Szabo’s theory of collectibles.

Nick Szabo’s contribution is foundational in a different register. In 1994 he defined the smart contract as:

“A computerized transaction protocol that executes the terms of a contract. The general objectives of smart contract design are to satisfy common contractual conditions, minimize exceptions both malicious and accidental, and minimize the need for trusted intermediaries. Related economic goals include lowering fraud loss, arbitration and enforcement costs, and other transaction costs.” — Nick Szabo, Smart Contracts (1994) [source]

His 2001 essay “Trusted Third Parties Are Security Holes” sharpened the argument: every time a trusted intermediary is introduced into a financial protocol, a vector for failure, censorship, or corruption is introduced alongside it. [source] Szabo developed the concept further in “Formalizing and Securing Relationships on Public Networks” (1997), describing digital agreements that could automatically execute and enforce terms using cryptographic protocols, covering property rights and multi-party arrangements without relying on institutional mediation. [source]

The implication for stablecoin exchange is direct: if smart contracts can enforce the money printer rules more resiliently than centralized institutions, and if the code is structurally indifferent to the identity of the counterparties it serves, then the question of whether privacy and security are mutually exclusive in digital currency exchange deserves re-examination.

The theoretical synthesis between code-as-governance and legal systems was formalized by Lawrence Lessig in Code and Other Laws of Cyberspace (Basic Books, 1999). Lessig’s core thesis: the absence of government regulation of the internet does not mean the absence of regulation considering that code written by software engineers provides the rules of interaction, embedding value judgments that set rules for how society interacts in cyberspace. Four modalities regulate behavior simultaneously: law, norms, market, and architecture. Of these, architecture (code) is the most effective online. [source] Lessig expressed concerns relative to code immutability.

Primavera De Filippi and Aaron Wright extended this analysis to blockchain in Blockchain and the Law: The Rule of Code (Harvard University Press, 2018), introducing the concept of lex cryptographia: rules administered through self-executing smart contracts that organize economic and social activity without depending on institutions or bureaucratic hierarchy. [source] Blockchain-based applications, they argued, both support and undermine existing laws, and the technology is poised to transform social and political institutions across payments (crypto banks), finance (AAVE), information systems (Polymarket), and organizational governance (Curve).

Immutable smart contracts represent the logical terminus of Lessig’s concern. If code is law and code is immutable, then the law is permanently fixed at deployment. This is not the internet Lessig feared, where private interests would capture the architecture. This is an architecture that has no owner. The consequences of this distinction were placed before a federal court between 2022 and 2025.

The Tornado Cash Verdict: Code as Legal Test

In August 2022, OFAC sanctioned Tornado Cash under Executive Order 13694, alleging it had laundered over $7 billion since 2019 — the first time OFAC targeted immutable smart contracts rather than individuals or centralized entities. The reversal came on March 21, 2025: OFAC officially lifted the sanctions, following a Fifth Circuit ruling that Tornado Cash’s open-source, self-executing software is not sanctionable. The court’s distinction: the rogue persons who abuse the protocol, not the code itself, are the proper objects of sanction. The ruling also applied Loper Bright v. Raimondo (2024), which overturned 40 years of Chevron deference, signaling courts may now read OFAC’s authority more restrictively against novel technologies. [source]

Hughes’ declaration that “Cypherpunks write code” survived a major legal test. The developer is not the user. The protocol is not the crime.

But this settlement does not resolve the harder question: are all protocols equal in this regard? The distinction between a neutral protocol and a harmful one is not found in the code itself — it is found in the specificity of purpose. A general-purpose privacy tool has a range of use cases spanning anonymous charitable donations to money laundering. A ransomware payment router has a single designed purpose. The Van Loon court implicitly adopted a proportionality principle, it is where the cypherpunk ethos and institutional compliance find their uneasy but workable boundary.

1.2 The Stablecoin Paradox: Sovereignty vs. Stability

The cypherpunk ambition was not merely private money — it was sovereign-independent money. Back’s Hashcash, Finney’s RPOW, Szabo’s Bit Gold, and ultimately Bitcoin were all attempts to create digital value whose credibility derived from mathematics and consensus, not from an issuing institution’s promise. The ideal was a currency that no government could debase, no bank could freeze, and no intermediary could deny. The stablecoin, in its dominant form, represents a considered retreat from this ambition: it achieves price stability by anchoring to the very sovereign currencies the cypherpunk movement sought to escape.

Fiat-Backed: The Centralization Bargain

USDC, USDT, and other fiat-backed achieve their pegs through a structurally simple mechanism: every token in circulation is backed by a dollar equivalent held in custody by a regulated institution. The on/off ramps require identity verification. Issuers are classified as financial institutions under the Bank Secrecy Act, subject to full AML and CTF obligations. Stablecoin holders have no direct claim to the underlying reserves, only a contractual right to redeem through the issuer on the issuer’s terms. [source]

The user who acquires stablecoins on primary markets enters the on-chain environment through a regulated gate. Once inside, the token is pseudonymous, the transfers are permissionless, and the code governs without asking for credentials. Once the user wishes to exit back to the real economy, the gate reappears. The privacy window is real but bounded at both ends by institutional infrastructure. The cypherpunk wins the middle leg; the regulators hold the entry and exit.

Algorithmic: The Cypherpunk Attempt and Its Failure Mode

The closer realization of the cypherpunk ideal was the algorithmic stablecoin — a peg maintained by code alone, with no custodian, no regulated reserve, no fiat counterparty. No gate. The ambition was a stable unit of account that derived its value entirely from cryptographic mechanism and market incentives, fully sovereign-independent.

History is a warning. Terra/Luna’s UST collapsed in May 2022, erasing approximately $40 billion in market value in under a week. [source]. Iron Finance’s TITAN had failed similarly in 2021. MakerDAO’s DAI survived its March 2020 Black Thursday near-collapse only through emergency governance intervention — a human backstop activating inside what was supposed to be an autonomous protocol.

The pattern is consistent: algorithmic stability mechanisms perform under normal conditions and fail catastrophically under stress, precisely because they lack the backstop that fiat-backed systems possess. The most sophisticated current approach, Ethena’s USDe, achieves near-stability through a delta-neutral synthetic: spot crypto collateral offset by short perpetual positions. But the mechanism depends on centralized exchange infrastructure for the short legs. The cypherpunk goal of a fully sovereign-independent stable unit of account has not yet been solved without introducing new trust vectors in its place.

Centralization as the Price of Real-World Adoption

This leaves the builder with a precise diagnosis. The upper DeFi layers can be permissionless. The base money layer, as long as the dollar is the reference, cannot be.

GHO, USDS, and similar crypto-backed assets attempt a middle path — on-chain issuance against crypto collateral, with redemption through smart contract mechanisms rather than regulated issuers. They avoid the fiat reserve requirement at the cost of capital efficiency and market risk. They represent lex cryptographia applied to money creation — and they remain outside the regulatory definition of a payment stablecoin precisely because of it.

A Light at the End of the Tunnel

The relevant question may not be permanent. The frequency with which a user needs to cross the fiat gateway is a function of how much of economic life can be conducted on-chain. That function is increasing. Employment is increasingly paid in stablecoins through DAO contributor structures. Commerce is settling on-chain. Borrowing, lending, and investment are available through DeFi without touching fiat rails. Tokenized real-world assets are growing from $5.8 billion at the start of 2025 to over $30 billion by late April 2026, collapsing the distance between on-chain and off-chain economic activity. [source]

The cypherpunk ambition may not require defeating the institutional layer — it may simply need to wait for the digital economy to grow large enough that crossing the fiat gateway becomes, for a meaningful portion of users, genuinely optional. At that point, the privacy question resolves not through regulation but through obsolescence of the chokepoint itself.

1.3 Who Uses Stablecoins: A User Taxonomy

On Methodology: The Volume Inflation Problem

Any attempt to measure stablecoin adoption confronts a methodological problem that must be stated before any figure is cited. On an adjusted basis — filtering out bots, wash trades, and other artificially inflationary activity — stablecoins processed $9 trillion in the last twelve months, up 87% year-over-year. Total unadjusted volume over the same period was $46 trillion. [a16z State of Crypto 2025] The ratio is roughly 5:1. Every headline claim that stablecoins have “surpassed Visa” uses the unadjusted figure. Visa’s own measurement methodology estimated approximately 10% of stablecoin transactions as genuine by their standards. [source]

On Solana and Base — where USDC supply dominates — unadjusted transactions represented over 98% of stablecoin activity as of December 2024, driven by memecoin launches and automated arbitrage strategies. [source] This segment generates significant volume data but represents protocol-native automation rather than a user category; it should not be scaled alongside consumer or institutional activity in any adoption metric without explicit adjustment.

A more honest signal than raw volume is velocity: the adjusted monthly transfer volume relative to circulating supply has roughly doubled since early 2024, climbing from 2.6x to 6x. [a16z] Rising velocity means existing supply is being transacted more actively — a more meaningful indicator of organic adoption than the nominal volume headline. With these caveats established, the user segments emerge clearly.

Segment 1: The Bankless User

The bankless user is the segment most directly aligned with the cypherpunk ambition, but not for ideological reasons. Their motivation is economic survival: accessing a stable store of value outside a banking system that is either unavailable, unreliable, or actively hostile to their interests. Capital controls, hyperinflationary local currencies, and exclusion from formal credit all produce the same behavior.

For this user, the cypherpunk properties of stablecoins are not political statements but functional requirements. The institutional compliance layer is not a philosophical objection; it is a practical obstacle.

The geographic and adoption dimensions of this segment are explored in Section 3. For the purposes of this taxonomy, the relevant observation is simpler: the bankless user demonstrates that the cypherpunk value proposition has a mass-market demand case that is entirely independent of ideological alignment.

The USDT dominance in this segment, via Tron, represents a structural disconnect relevant to any exchange protocol: the chain used for grassroots stablecoin adoption is not the chain where DeFi clearing and settlement infrastructure operates.

Segment 2: Illicit Use

Stablecoins are not a meaningful medium of exchange for darknet commerce. Darknet markets are dominated by Monero (60% of activity in 2025) and Bitcoin, for reasons of structural necessity: privacy-by-default and untraceability are prerequisites for goods-and-services exchange in that environment. [source] Most stablecoins are structurally unsuitable.

The stablecoin illicit exposure that does exist is concentrated in post-hack laundering flows, and the mechanism reveals a structural problem that is distinct from, and more interesting than, simple criminal use. Consider the following sequence: Alice deposits fiat to mint a stablecoin and provide it to a liquidity pool. The pool is exploited. The hacker routes the stolen stablecoins for ETH or BTC before disappearing into opaque CEX accounts or mixing infrastructure. The fiat that Alice contributed to mint those stablecoins has now effectively backstopped the hacker’s conversion into an untraceable asset. The issuer’s reserves remain intact but the on-chain claim to that backing has transferred to a bad actor who has since poisoned the pool entirely.

Segment 3: The Institutional and Derivative Layer — Mechanisms and Fair Exchange Rates

The most analytically underserved segment is institutional users, where stablecoins function not as payment instruments but as denomination layers for structured financial products. The mechanisms of the protocols serving this segment differ substantially, and those differences bear directly on what a fair exchange rate between them should be.

The use patterns make this clear. Stablecoins serve as the liquid leg in yield-bearing structured products: sUSDe (Ethena’s staked wrapper) offers funding-rate yield; USD0++ (Usual) offers T-bill duration exposure with a four-year lock; BUIDL (BlackRock) tokenizes a money market fund and distributes daily dividend accruals on-chain — its secondary use as collateral for leveraged DeFi positions has driven demand well beyond its original treasury management intent. [source]

For this segment, the relevant question when exchanging stablecoins is not “will I get my dollar back” but “am I getting the correct risk-adjusted price for the instrument I am exiting and the one I am entering.” A swap from sUSDe to USDC is not a dollar-for-dollar exchange — it is an exit from a yield-bearing synthetic position into a regulated reserve instrument with different counterparty risk, different redemption mechanics, and a different regulatory classification. We develop a benchmark on how to measure fair exchange rates between stablecoins in Section 2 of this paper.

1.4 Individual Autonomy: Between Centralization and Decentralization

The cypherpunk thesis and the institutional compliance framework do not resolve in either direction in the stablecoin ecosystem. They resolve into a layered topology.

At the base layer — issuance, reserve management, fiat convertibility — institutional control is structurally necessary and, for as long as the dollar is the reference peg, not escapable. The Terra/Luna lesson is precisely this: the absence of a real-world backstop is not a feature of sovereignty but an unpriced tail risk.

At the transfer and holding layer — dApps, DEX routing, self-custody — the code is law, in the precise sense that Hughes, Back, Finney, Szabo, De Filippi, and the Van Loon court all described. The protocol cannot ask for your identity. The contract executes against its conditions, not against its users’ credentials. The permissionlessness of this layer is not an accident of regulatory gap; it is a deliberate architectural feature that the GENIUS Act explicitly chose not to regulate.

Individual autonomy in this ecosystem exists at the interface between these two layers, preserved in proportion to how little the user depends on regulated intermediaries, and how much of their economic life can be conducted without touching the fiat gateway. For builders, the practical question is not about compliance, it is about design intent. The degree of institutional entanglement built into an exchange protocol determines where on this topology it sits, and therefore which user categories it can serve, what privacy it can preserve, and what trust model it requires from its counterparties.

Section 2: The Fungibility Issue

2.1 — Is 1:1 Accurate?

Section 1 established that stablecoins operate across a layered topology: the base money layer is centralized by necessity, the transfer and holding layer is permissionless by design. The question Section 2 dives into what happens inside that permissionless transfer layer — for any holder executing a swap, and for any protocol positioned within that market. Not whether stablecoins can move freely, but whether they move at fair value when they do.

The answer is structurally no. The 1:1 exchange rate between stablecoins is a convention that holds in aggregate and breaks at the margin for every individual transaction. Understanding why this is unavoidable, and what it implies, is the subject of this section.

Embracing the Chaos of On-Chain Peg Inefficiencies

Gorton and Zhang’s “no-questions-asked” principle opens the argument correctly, provided its limits are stated immediately. The NQA failure is not a market failure. Price adjusts continuously to the information available at any given moment, not punctually, not only during identifiable stress events, but proportionally and permanently, tracking the market’s evolving perception of risk. The stablecoin market is not broken when a 5bps spread appears between USDC and USDT on a Curve pool at 2am on a Tuesday. It is doing exactly what it should.

The problem is that the market is structurally over-sensitive. Small information signals produce disproportionate micro-deviations. Small liquidity imbalances produce outsized spreads. The end user bears the full cost of this sensitivity on every swap, paying the market’s uncertainty premium regardless of whether they have any view on, or access to, the underlying information driving it.

Embracing this chaos is not a passive stance. It is the recognition that local inefficiency in stablecoin pricing is permanent and structurally unavoidable: no amount of reserve transparency reform, regulatory standardization, or liquidity deepening eliminates the continuous repricing that characterizes any multi-issuer, multi-chain, multi-collateral market. Controlling the chaos means building an architecture that is resilient to it, one that absorbs friction transparently, on-chain, and serves the end user at correctly-priced rates rather than exposing them to the full volatility of the market’s moment-to-moment adjustments. The chaos does not disappear. It is handled backstage.

Gorton, G.B. & Zhang, J.Y. (2023). “Taming Wildcat Stablecoins.” University of Chicago Law Review, 90, 909. [SSRN 3888752]

Reserve Divergence: A Framework for Fair Rate Benchmarking

Every major stablecoin claims par value against the US dollar. The divergence in what backs that claim — and in how observable, how liquid, and how accessible that backing is — is the source of the structural spread. A benchmark for fair exchange rates between stablecoins must therefore decompose the peg claim into three measurable risk dimensions.

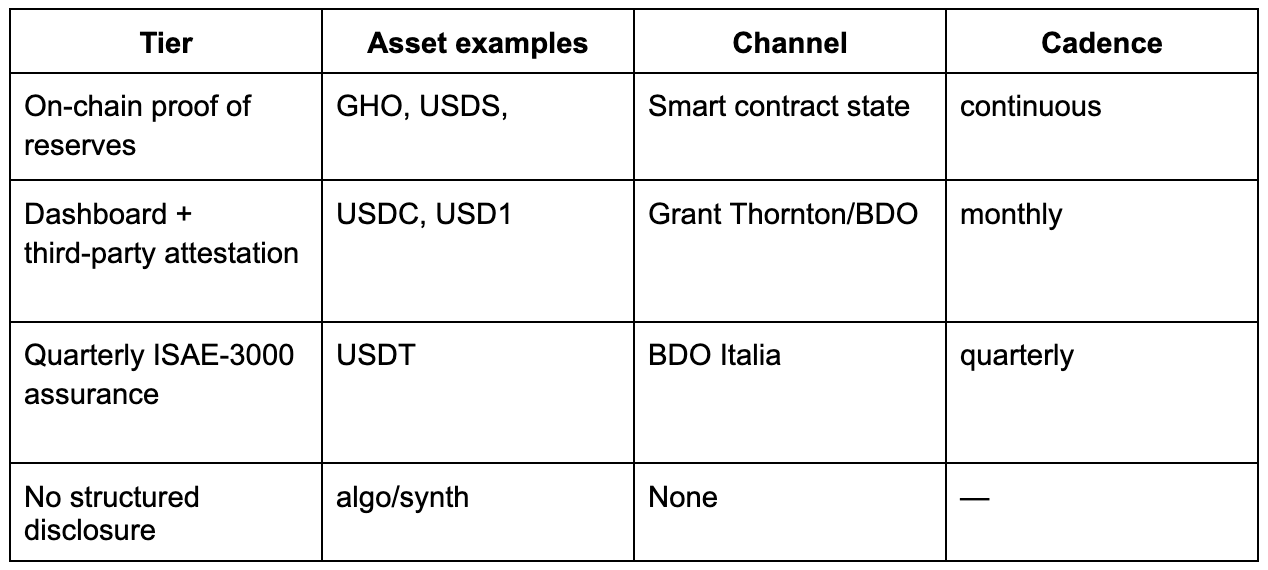

Layer 1 — Information Asymmetry: The Transparency Discount

The first variable is what a market participant can know about a stablecoin’s backing at the moment of the trade, with what latency, through what channel.

The transparency hierarchy, in descending order of verifiability:

The market prices these tiers as a discount gradient. The information lag between an issuer’s actual reserve state and the market’s knowledge of it ranges from zero (on-chain proof) to three months (quarterly assurance). This lag is what the market prices as an opacity premium — a persistent basis between assets with equivalent nominal claims but structurally different verification latency. [source: tandfonline.com/doi/full/10.1080/1351847X.2025.2505757]

An entity operating at the intersection of multiple stablecoins with active access to on-chain redemption paths — GSM, PSM, fiat rails — observes the actual redemption rate in real time rather than depending on public attestation cadence. Combined with established KYB relationships enabling direct access to issuer fiat redemption channels, the information asymmetry that creates a spread for the average market participant is structurally smaller for such an entity.

Layer 2 — Risk Layers: Smart Contract, Market, and Operational

Smart contract risk is primarily a venue-level variable for fiat-backed stablecoins with simple, audited ERC-20 contracts. It becomes an asset-level variable for stablecoins with on-chain backing mechanisms — GHO positions locked in Aave V3, USDS CDP logic in Sky — and for any yield-bearing wrapper where contract logic directly affects redemption value. The benchmark should flag this distinction.

Market risk should be proxied through two observable variables without requiring live position data. First, the quality of market support: a CEX actively quoting the asset as a base pair is the strongest signal of genuine market maker engagement as it implies order book depth, price discovery independent of on-chain pools, and competitive spread maintenance by professionals with real inventory. Second, the share of supply emitted through recursive lending loops — assets borrowed against collateral that itself was borrowed — which carries no organic demand and exits simultaneously under any stress event, making apparent liquidity illusory.

Operational risk is the category with the highest consequence for smaller issuers and the least standardized measurement methodology. The relevant targets are not the largest stablecoin issuers since they have scale, legal infrastructure, and regulatory standing that make default probability low regardless of other concerns. The more interesting case is the category of smaller stablecoin issuers that seek depth and stability not through their own scale, but by integrating into larger stablecoin ecosystems. For these issuers — whose resilience depends on the composability and liquidity access granted by connecting to a unified layer of higher-tier assets — operational risk is measured through governance transparency (on-chain vs. opaque multisig), team and budget accountability (public DAO forum vs. undisclosed corporate structure), and compliance trajectory (licensed vs. informally operating). The relevant metric is not default probability but the probability of an operational event — governance capture, key-person risk, regulatory action — that disrupts the redemption mechanism independently of collateral quality.

Layer 3 — Barriers to Redemption Access

Redemption access carries a cost, and that cost belongs in the benchmark. The cost structure varies across a wide range: some paths are permissionless, zero-fee, and executable on-chain; others require minimum transaction sizes, identity verification, or institutional relationships unavailable to the majority of holders.

This access asymmetry means the fair exchange rate is not uniform across market participants. It is a function of who is executing the swap. A B2B actor operating at scale accesses structurally narrower redemption economics than a retail holder navigating the same landscape.

“Circle typically only redeems with a set of institutional customers; Tether with an even smaller set. Interestingly, under MiCa in Europe, stablecoin issuers are required to offer redemptions to all customers.” A great boost to Euro stablecoins.

The Benchmark

A fair market rate between stablecoin A and stablecoin B is therefore:

where:

I =Info discount

R = Risk premium

C = Access cost

where each variable represents the market’s real-time pricing of the corresponding friction layer. Under normal conditions this resolves to 1–15bps between major stablecoins, the correct price of exchanging one imperfect claim for another. Under stress it widens to reflect realized friction rather than theoretical parity.

Any protocol capable of performing efficient arbitrage on structural depeg events can provide a proper clearing infrastructure for stablecoins — pricing the spread correctly, absorbing the flow, and distributing the economics to those who make it possible rather than allowing it to leak into extraction.

The structural corollaries: USDT bears wider structural spread due to reserve opacity and access barriers, USDC-equivalent risk profile becomes the de facto terminal layer for on-chain redemption networks, RWA-backed assets ; are developed further in Section 2.2.

Small and Chronic: The Everyday Depeg

The fungibility problem is not primarily a crisis event problem. It is a volume problem operating silently across millions of daily transactions.

Under best conditions on a deep, balanced pool, a USDC→USDT swap achieves sub-3bps of combined fee and slippage. This is the wholesale rate: available to a well-routed trade on the deepest pool, on the right chain, at a moment of pool balance, with no MEV exposure and fresh oracle state. Every deviation from these conditions widens the spread. In practice, stablecoins deviate 5–8bps from their nominal peg every day across on-chain pools with no stress event, driven by pool rebalancing flows, oracle update latency between block boundaries, and liquidity fragmented across chains and fee tiers.

Within this 3–8bps range, billions of dollars are processed between stablecoins. The spread does not disappear, it is extracted: by LPs absorbing impermanent loss against informed arbitrage flow, by MEV bots front-running predictable swaps, and by fee tier misrouting across fragmented pools. Annual losses for traders from sandwich extraction alone are estimated at approximately $60 million, with block builders capturing most of this value. [source: eigenphi / arkm.com MEV data 2025]

Research in this space is converging on several approaches to reduce this leakage. RFQ-based execution connects traders directly with professional market makers quoting firm spreads from inventory, [source: eco.com OTC vs RFQ] Intent-based protocols with CoW Swap’s batch auctions, 1inch Fusion’s Dutch auction resolvers — match opposing flows within a batch before touching on-chain liquidity, removing public mempool exposure and neutralizing the primary MEV vector. [source: dextools.io CoW Swap guide] At the block-building level, Titan and BuilderNet together produce over 85% of Ethereum MEV-Boost blocks — meaning the infrastructure that extracts value from stablecoin swaps is already concentrated enough that privileged order flow agreements can redirect rather than merely avoid extraction. [source: relayscan.io builder data]

These approaches narrow the spread for users who can access them at the right trade size. None of them solve the underlying distribution problem. The conditions required to achieve best execution — correct pool, correct chain, correct routing, MEV protection, oracle freshness, minimum trade size for RFQ access — must be met simultaneously. Across a population of stablecoin holders, the distribution of sophistication, capital size, chain access, and routing awareness means the vast majority execute at materially worse than wholesale rates. The spread between wholesale execution and median retail execution is not a technical failure awaiting a fix. It is a structural feature of any fragmented, multi-asset, multi-chain market.

What this section addresses is the mechanical anatomy of that spread: oracle feeds and latency between block boundaries, impermanent loss as a structural tax on AMM liquidity, and slippage as an unavoidable consequence of fragmented pool depth. Understanding the mechanics of the spread is the precondition for understanding what it would mean to price it correctly.

The Lyons Framework: Arbitrage as the Peg Mechanism

Lyons and Viswanath-Natraj establish the foundational result: stablecoin issuance — the closest analogue to central bank intervention — plays only a limited role in peg stabilization. The peg is maintained by demand-side arbitrage: private actors closing the spread between secondary-market price and peg, depositing when the stablecoin trades at discount, withdrawing when at premium. [source: NBER WP 27136] Improved arbitrage design is what demonstrably reduces peg deviation over time.

“Lyons, R.K. & Viswanath-Natraj, G. (2023). ‘What Keeps Stablecoins Stable?’ Journal of International Money and Finance, 131, 102777.”

The value arbitrage captures is the spread between the secondary-market price and the peg. A holder who sold a depegged stablecoin at $0.97 paid the arbitrageur $0.03 to exit their exposure. That $0.03 represents the risk premium the market demanded — the cost of holding an asset whose peg was in question.

The relevant observation for a trader is different: that spread could, under different routing conditions, be retained rather than surrendered. The spread is not eliminated. It is allocated correctly, and the question of who it accrues to is a question of protocol design, not of market efficiency.

This reframes the problem from Section 1’s cypherpunk/compliance axis onto a market structure axis: the stablecoin market is not short of privacy, not short of liquidity. It is short of infrastructure that prices friction correctly for end users and returns the surplus to those generating the volume.

Section 2.2 — Quality vs Toxic Arbitrage

Section 2.1 established that stablecoin clearing is, under the hood, an arbitrage product — pricing the spread between two imperfect claims, absorbing flow at correctly-priced rates, and distributing the economics of that position rather than allowing it to leak into extraction. The question that follows is what kind of arbitrage actually operates in the stablecoin market, who runs it, and what information gates its execution.

The section narrows to a single instrument: oracle feeds as the on-chain measurement of how far an asset trades from its benchmarked target rate at the moment of exchange. The distinction between quality and toxic arbitrage is the lens. The conclusion is about what a properly designed clearing operator is exposed to.

Quality vs Toxic Flow

The distinction is mechanical, not moral.

Quality arbitrage ensures that asset A on pool 1 prices the same as asset A on pool 2. A deviation appears somewhere — on a DEX pool, across chains, between a CEX price and a DEX quote. The arbitrageur is reactive: they observe the deviation and backrun the orderflow that created it, closing the spread between the two venues. The common thread across all quality arbitrage — CEX/DEX, DEX/DEX, cross-chain — is that it is convergent. After the trade, the two prices are closer together than before. The trader who created the deviation does not interact with the arbitrageur at all. Lyons and Viswanath-Natraj identify this as the primary peg-stabilization mechanism: the actor capturing the spread is also the actor restoring it. [NBER WP 27136]

Toxic flow operates on the opposite logic. Rather than reacting to a deviation that already exists, it manufactures one by frontrunning a pending trade. The mechanism: a bot identifies a user transaction in the public mempool, observes their slippage tolerance, and uses gas priority or flashloan-backed capital to execute ahead of them, moving the price to the edge of what their parameters allow, letting their trade execute at the worst acceptable rate, then close the position to realize profit. The user’s slippage tolerance is the attack surface. The toxic arbitrageur does not correct any price discrepancy; no convergence occurs. The only output is a transfer of value from the trader to the extractor, with the block builder capturing the gas premium that made the ordering possible.

The end user can distinguish between these outcomes post-execution. Quality flow leaves the trader’s realized rate at or near the benchmark. Toxic flow leaves a measurable gap between the pre-execution quote and the realized rate. The difference is observable in execution data and is the correct empirical basis for classifying flow type at scale.

Oracle Feeds as Information Vectors

The oracle price is the on-chain representation of how far an asset currently trades from its benchmark target rate. It does not set the price but it reports what the market believes the price is at the moment of the update. When the oracle price of stablecoin A diverges from $1, this is not a feed failure. It is an accurate encoding of market sentiment. The oracle is the instrument that makes this divergence legible on-chain to any system requiring a real-time signal of whether an asset is trading at, above, or below its benchmark at the moment of execution.

Current infrastructure supports sub-second price refresh at deviation thresholds tight enough to capture meaningful stablecoin basis in real time. The technical ceiling on oracle precision is not a binding constraint for assets with active, continuous price discovery. The relevant variable is the magnitude and persistence of the divergence the oracle reports because that determines what class of arbitrage opportunity exists and for how long.

This divergence defines two regimes:

Seconds-scale: A local pool imbalance creates a transient deviation that the oracle registers before on-chain arbitrage closes it. From the perspective of a trader executing via a properly designed clearing operator, this regime does not affect their quote quality. The oracle identifies the local deviation; the routing absorbs it and returns the spread to the trader at execution rather than leaking it to reactive bots. The trader should receive a better rate than the open market offered at that moment.

Hours-scale: A macro-supported deviation (a reserve transparency event, a governance shock, a sustained redemption queue imbalance) persists across multiple blocks and multiple oracle updates. The oracle continuously reports sub-peg pricing for an extended window. This is the duration regime within which quality arbitrage capital can position and execute at scale, and within which the spread between market price and benchmark accumulates enough depth to matter for capital allocation decisions.

The oracle feed is the gate. A system anchored to oracle divergence from benchmark activates when the feed confirms that an asset is trading away from its target rate, and is inactive when it is not. It is not a general-purpose swap venue. It is a market participant that exists specifically in the space opened by the oracle’s signal and does not process volume when that signal is absent.

The LP Argument: AMM Curves and Their Structural Costs

Passive AMM liquidity providers in stablecoin pools face two structural costs that are not optional features of their position but consequences of the AMM curve itself.

The first is impermanent loss embedded in the bonding mechanism: any trade that rebalances the pool moves it along the curve, leaving the LP holding more of the asset that depreciated and less of the one that appreciated. In stablecoin pools during depeg events, this effect is directional and asymmetric, the LP accumulates the depegging asset as its market value falls, because the AMM curve forces them to absorb the selling pressure that quality arbitrage generates (that arbitrage becomes toxic to the LP). .

The second is LVR — loss-versus-rebalancing: the adverse selection cost arising from the information gap between passive LPs and informed arbitrageurs. LVR captures costs incurred by AMM LPs due to stale prices that are picked off by better-informed arbitrageurs. Adverse selection occurs because HFTs have access to real-time market prices that passive LPs do not, enabling them to execute top-of-block arbitrages between stale DEX prices and live market prices at the LP’s expense. LP losses to arbitrageurs exceed fees earned across many of the largest AMM pools, and CLMM LPs (Uniswap v3) perform worse than constant-product LPs on an LVR-adjusted basis since concentration amplifies the cost of capital.

Both costs are structural consequences of the AMM curve forcing the LP into a passive, always-on quoting posture against any flow the market sends. The correct hedge against these costs — for any entity that takes the counterpart side of stablecoin exchanges — is not better pool parameterization. It is proper inventory rebalancing: actively managing the composition of the held basket in response to flows received. LVR formalizes exactly this: the LP’s loss is the arbitrageur’s gain because the LP cannot rebalance at market prices between trades.

A proper clearing operator is not exposed to IL and LVR in the way passive AMM LPs are. The distinction matters because it changes the economics of the position entirely: the clearing counterpart’s cost of capital is a function of its rebalancing efficiency, not of the AMM formula it is subject to.

Milionis, J., Moallemi, C., Roughgarden, T. & Zhang, A.L. (2022). “Automated Market Making and Loss-Versus-Rebalancing.” arXiv:2208.06046. [link]

Section 3: Forex & Adoption

Section 2 mapped the mechanics of stablecoin exchange through the fungibility problem, the spread between imperfect claims, the infrastructure gaps that prevent any individual participant from consistently transacting at fair rates. Section 3 steps back from the mechanics and asks what this market is actually doing to the world economy. Not how stablecoins are priced, but where they are going, who is using them, and what they are displacing.

The answers are incomplete. This section operates as a thought experiment rather than a demonstration. The dynamics are live, the data is partial, and the direction of travel is clearer than the destination.

3.1 — The Dollar Monoculture

Traditional foreign exchange is a two-currency system in practice. The US dollar sits on one side of approximately 90% of all FX transactions. The euro participates in 38%. These two currencies co-dominate global trade invoicing, reserve holdings, and cross-border settlement. They do not dominate equally, but the distance between them and everything else is enormous.

On-chain, this ratio collapses into near-total dollar monoculture. Stablecoins pegged to the US dollar represent 97% of all stablecoin issuance. The remaining share consists mostly of euro-denominated stablecoins. As of January 2026, euro-denominated stablecoins carry a market capitalization of approximately €450 million which represents less than 1% of the global stablecoin market. European stablecoins account for 0.35% of DeFi’s total stablecoin supply.

The euro’s near-absence on-chain is not primarily a builder preference. Two structural factors explain it.

Regulatory sequencing: Europe moved earlier and more comprehensively than the US on stablecoin regulation, but MiCA’s pre-enforcement period suppressed the category before clarifying it. Following MiCA’s full implementation in December 2024, European exchanges delisted over $140 billion worth of non-compliant stablecoins, primarily USDT. Euro stablecoin supply growth since then correlates almost perfectly with regulatory enforcement rather than organic market demand. The market grew not because users demanded euros on-chain but because regulators removed non-compliant alternatives in European jurisdictions. Euro stablecoin market capitalisation more than doubled in the 12 months after MiCA’s June 2024 rollout.

DeFi liquidity bootstrapping: DeFi protocols are built around dollar-denominated pricing. Yield strategies, lending markets, and collateral frameworks assume USDC or USDT as the base asset. A euro stablecoin entering this ecosystem faces a structural cold-start problem: liquidity attracts users, users attract liquidity, and neither materialises without the other. MiCA compliance is necessary but not sufficient, euro stablecoins also need a DeFi primitive to anchor demand equivalent to what Curve’s 3pool did for USDC and USDT. EURC leads at $445M market capitalisation but has shallow liquidity pools. EURe shows higher transaction volume but restricted market reach. Scattered liquidity pools and weak adoption patterns impede expansion.

Beyond the euro, alternative currency breakthroughs remain nascent. BRZ (Brazilian real, Transfero) is the most technically developed non-dollar/non-euro stablecoin — multi-chain, compliant, reserve-backed — and its market cap is measured in tens of millions. BRL-pegged stablecoin trading volume reached $906 million in H1 2025 — a rounding error against USDT’s daily volume exceeding $100 billion. IDRX (Indonesian rupiah) and PHPC (Philippine peso) exist as proofs of concept. None has crossed the liquidity threshold where it functions as a genuine on-chain currency rather than a niche settlement instrument.

Populations most exposed to currency instability are adopting digital dollars, not digital versions of their own currencies. Brazil has the most sophisticated local-currency stablecoin infrastructure of any emerging market but its millions crypto-exposed users are integrating into dollar-denominated rails.

The cold-start problem for non-dollar stablecoins is partly a liquidity problem and partly an infrastructure problem. A clearing layer that holds inventory across multiple currency denominations and prices exchanges at fair rates could offer a more direct path between any two stablecoins, including non-dollar pairs. Broader currency coverage in the clearing layer translates to lower conversion costs for the end user and potentially to deeper organic demand for non-dollar denominations.

3.2 — The Dollar Rotation: Strategy or Gravity?

The convergence of on-chain activity toward the dollar is occurring through two distinct mechanisms that are often conflated.

Accidental dollarization — the survival behavior channel: Populations in high-inflation economies are not choosing dollar hegemony. They are escaping local monetary failure, and the only available digital stable asset with sufficient liquidity happens to be dollar-denominated. The academic literature now has a name for this: “digital dollarization.” [source] The dollarization is a byproduct of rational individual behavior under monetary stress, not a coordinated policy outcome. Venezuela conducts significant daily commerce in USDT without any formal dollarization policy. Argentina and Turkey show the same pattern. The local currency survives as legal tender for wages and taxes; the stablecoin captures the transactional and savings layer.

Deliberate strategy — the cryptomercantilism channel: The current US administration has framed this explicitly as a strategy of “cryptomercantilism” — stopping CBDC projects while pushing USD stablecoins to reinforce the international use of the dollar for payment and invoicing through private infrastructure. The GENIUS Act is the legislative instrument: by mandating Treasury-backed reserves for all regulated stablecoin issuers, it converts global stablecoin adoption into demand for US government debt. Tether and USDC already collectively hold more US Treasuries than Saudi Arabia. With Standard Chartered projecting stablecoin supply at $2 trillion by 2028, the GENIUS Act channels demand for Treasury securities through end users worldwide. Whether this materially reduces the cost of US debt financing is contested — it is not a fiscal panacea given the scale of $30 trillion in outstanding Treasuries — but the directional effect is real and the incentive to preserve it is significant.

The same rails cut both ways: The infrastructure that reinforces dollar dominance for compliant users simultaneously provides plumbing for actors seeking dollar access outside regulated channels. Russia began using stablecoins for international payments following legislative changes specifically designed to counter Western sanctions. Sanctioned entities route through permissionless on-chain infrastructure precisely because it cannot refuse them at the code layer. Wide adoption of US dollar stablecoins means the privatization of global seigniorage.

The on-chain RWA extension: RWA trading on Hyperliquid reached a record 47.1% of total platform volume in April 2026, with HIP-3 enabling permissionless deployment of perpetual contracts on tokenized commodities, equity indices, oil, and gold. USDC is Hyperliquid’s aligned quote Asset, the base denomination for all markets on the platform. As on-chain RWA markets mature, a trader anywhere with platform access can gain exposure to gold, oil, equity indices and stocks all settled in USDC, without distinction. The dollar does not need to be physically present to exercise monetary gravity.

As on-chain finance expands to encompass RWA trading, cross-border settlement, and programmable payment flows, the natural next question is what sits at the centre of these exchanges. A clearing layer capable of processing fair forex exchanges on-chain would occupy a structurally important position in this stack, as the neutral infrastructure that funnels locally quoted assets into a unified dollar based exchange layer.

Weak currencies — bifurcation, not a race: Currencies with institutional backing and political capital to defend monetary sovereignty are building their own digital infrastructure. They are not surrendering. The euro appreciating significantly against the dollar in 2025, with record inflows into European government bonds, is the counter-signal. China’s mBridge project enables cross-border CBDC payments without dollar intermediation.

Currencies without those resources are surrendering through population behavior, not policy. The relevant question is no longer whether the Argentine peso or the Nigerian naira survive as legal tender, they may, for tax and wage purposes. It is whether the state retains any effective monetary policy transmission when the population conducts economically meaningful activity in a parallel dollar-denominated digital layer. The evidence from Venezuela suggests the answer is: barely.

3.3 — Consumer Use Cases and Regional Integration

The geography of stablecoin adoption maps onto a simple inversion: the regions with the highest volume-per-transaction have the lowest population penetration, and vice versa.

Asia-originated B2B stablecoin payments lead at $245 billion annually, driven by Singapore, Hong Kong, and Japan. North America follows at $95 billion. Europe at approximately $50 billion, compliance-first under MiCA. Latin America and Africa together account for less than $1 billion in formal B2B stablecoin payment volume but represent the highest-growth trajectories and penetration. An estimated 66% of global stablecoin supply is held by individuals in emerging markets.

Latin America is the most advanced region on implementation: 100% of surveyed financial institutions are either live, piloting, or in planning with stablecoin payment infrastructure. 92% report their wallet and API stack is ready. The integration has moved beyond fintech pilots into mainstream consumer products: Nubank serves over 100 million users with stablecoin-adjacent functionality; Mercado Pago has deployed stablecoin settlement rails across six countries; Stripe extended stablecoin payment infrastructure to Latin American merchants in late 2025.

Most regulated: Europe under MiCA, the most comprehensive stablecoin framework globally, followed by Hong Kong’s Stablecoin Ordinance (May 2025) and the US GENIUS Act (July 2025).

Most builder-dense: The US and Europe by number of protocol teams. Southeast Asia by institutional payment infrastructure. Latin America by the fastest-growing developer base relative to its starting point.

The missing piece in both stories is conversion. A user in Lagos holding USDT and a merchant in São Paulo quoting in BRL need a conversion layer that is fast, and cheap. A user in Buenos Aires receiving a remittance in USDC and paying locally in a different denomination needs the same. Today that conversion leaks to spread, to exchange fees, to friction that was never designed for this use case. A clearing operator embedded into payment and cross-border channels processing conversions at the lowest operational cost, accessible at both the retail and institutional level, is not a marginal improvement on the existing stack.

Conclusion

The cypherpunk inheritance and the institutional reality did not cancel each other out in the stablecoin industry, they settled into layers. The base money layer is centralized by necessity. The transfer layer is permissionless by design. What sits between them, for any user navigating the stablecoin ecosystem, is a continuous friction cost that no individual participant can eliminate on their own and that the current market structure extracts rather than prices.

Stablecoins claiming identical pegs are not the same instrument. Their backing diversity, transparency gaps, and redemption barriers encode a spread that is captured by MEV infrastructure, absorbed by passive liquidity providers who systematically undercharge for it, and leaked through oracle latency. The friction to adoption is real: the regions with the deepest stablecoin penetration relative to GDP are precisely the regions where conversion infrastructure is most absent and where the cost of that extraction falls hardest.

A solution comes in the form of an hybrid on/off-chain clearing operator that would:

safeguard the privacy of users,

serve both retail and institutional users

align builders by reducing composability friction across stablecoins

settle exchanges at rates that reflect accurate target value

This is not a product sitting on top of the stablecoin market. It is the infrastructure layer that makes the stablecoin market competitive for issuers, for liquidity providers, and for the end users.

The stablecoin economy is a prelude. To what, exactly, remains the question. Whether stablecoins are accelerating the shifts in the global monetary order or whether those shifts are driving stablecoin adoption is the chicken-and-egg this paper can not resolve. The rails to exchange value and price information on-chain now exist. The experiment is running. What it produces will depend, in no small part, on who builds the infrastructure that sits at its centre.

Opening

The imaginative work on stateless money, on currency without a sovereign, on exchange without a gatekeeper, was done before the infrastructure to make it real existed. From Asimov’s Foundation credits to the Galactic Standard of George Lucas, science fiction assumed civilisations at scale converge on a common unit of account whose legitimacy comes from the network, not the issuer. Dune gave the political dimension: whoever controls the store of value controls the terms of every other exchange, and great powers converge not on ideology but on scarcity. Ghost in the Shell asks when an information pattern acquires the reality of the thing it represents. Blade Runner shows what fills the space between state jurisdiction and enforcement capacity. Cryptonomicon made the argument this paper opened with: privacy and monetary sovereignty are the same problem, and the people who understood that built the tools.